Home Battery Financing Options in Australia (2025–26)

Not everyone has $8,000–$15,000 sitting in an offset account for a home battery. The good news: there are several legitimate financing paths, and the right one depends on your situation. Here's how to evaluate the options without getting trapped in expensive financing.

Option 1: Cash (Offset Account or Savings)

The default advice: if you have cash sitting in a mortgage offset or high-interest savings account, using it to fund a battery purchase may actually make sense.

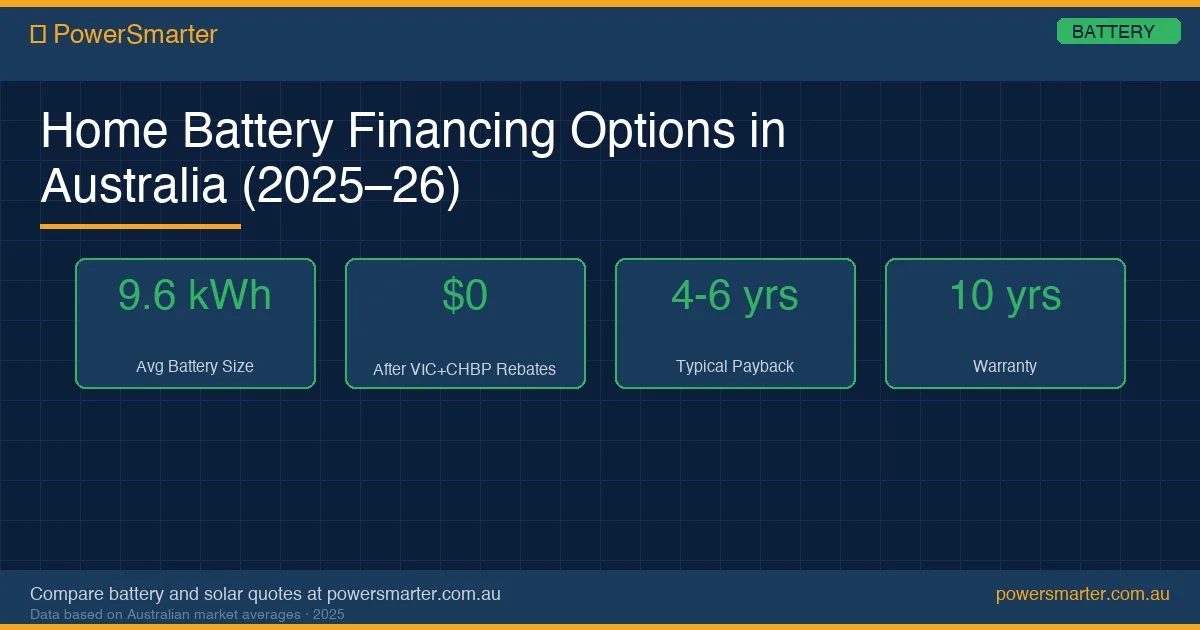

Your offset account is effectively earning your mortgage interest rate — say, 6.5%. A well-designed battery system returning $1,200–$1,800/year on an $8,000–$10,000 net cost delivers a 12–18% financial return in the first years (including the CHBP rebate impact on cost). That beats your offset account earnings.

The caveat: this only holds if the battery is genuinely well-suited to your household's usage. Don't withdraw offset funds for a battery that doesn't financially stack up.

Option 2: Green Home Loan / Mortgage Redraw

Several Australian lenders offer green home loans or allow redraw from an existing mortgage at home loan interest rates (currently 5.5–7% for most borrowers). Funding a battery through your mortgage at 6% is much cheaper than a personal loan or BNPL arrangement.

The consideration: you're adding to your home loan and paying interest over the life of the loan. If you redraw $10,000 and take 5 years to repay it at 6.5%, total interest cost is around $1,700. That's manageable given the battery savings you're generating.

Several lenders have specific green home loan products (Commonwealth Bank Green Home Offer, NAB, ANZ) that sometimes offer better rates for energy efficiency upgrades. Worth checking if you're a customer.

Option 3: Personal Loan (Green Loan)

A number of Australian lenders — including Clean Energy Finance Corporation (CEFC) backed programs via credit unions and smaller lenders — offer "green" personal loans for solar and battery at competitive rates (currently around 6–8% for strong credit). These are often unsecured, so they don't require home equity.

Compare rates on Canstar or Finder before committing. The spread between the cheapest and most expensive personal loans for the same purpose can be 5+ percentage points.

Option 4: Installer Finance (BNPL / In-House)

Many installers offer finance through BNPL partners (Humm, Brighte, Plenti) or their own in-house finance programs. The pitch is attractive: "Nothing to pay upfront." But read the terms carefully.

Key questions:

- What's the interest rate after any promotional period? (Can be 12–26% for some BNPL products)

- Are there early repayment fees?

- Is the financing rate baked into an inflated system price?

Some installer finance is reasonable — Brighte Green Loans, for instance, often offer competitive rates specifically for solar and battery. Others are expensive consumer credit dressed up as a solar benefit. Get the rate in writing and compare it to alternatives.

Option 5: Battery-as-a-Service

BaaS models have no upfront cost. Instead, you pay a monthly or per-kWh fee for using the battery, which is owned and maintained by the provider. This can work if you're cash-constrained and the net monthly saving (bill reduction minus BaaS fee) is positive from day one.

The downside: you don't own the asset at the end (in most models). You're paying for energy savings, not building equity in hardware. Check exit clauses carefully — particularly what happens if you move house.

How Financing Changes the ROI

A battery that delivers $1,500/year in savings and costs $9,000 net (post-CHBP) has a 6-year payback period on a cash basis. With a 7% personal loan over 5 years, you pay approximately $1,900 in interest — extending the break-even to around 7.3 years.

That's still within the 10-year warranty period, so financing still makes sense economically in this scenario. The key is not to finance at high rates (above 10–12%) for a system with borderline savings — the interest can push payback past the warranty window.

The Clean Energy Finance Corporation

The CEFC has programs that support household renewable energy financing through partner lenders. These programs are designed to make green finance cheaper and more accessible. If you're struggling to find competitive rates, the CEFC website lists current programs and participating lenders.

The Bottom Line

In order of preference:

- Cash / mortgage offset (cheapest, no interest)

- Mortgage redraw at home loan rate (cheap if you have equity)

- Green personal loan through CEFC-backed lender (competitive rates)

- Standard personal loan at competitive rate (manageable if under 8%)

- Installer BNPL / in-house finance (check the rate — can be expensive)

- BaaS (good for cash-constrained, but you don't own the asset)

Comments (0)

No comments yet. Be the first to share your thoughts!